What is AML?

Anti-money laundering (AML) refers to a set of procedures, laws and regulations designed to stop criminals from generating income through illegal actions. Directives such as the Bank Secrecy Act (BSA) in the U.S. require financial institutions to prevent, detect, and report money laundering activities. Though anti-money laundering laws cover a relatively limited number of transactions and criminal behaviors, their implications are far-reaching. AML screening software lets companies meet their regulatory requirements by helping to keep money launderers away.

Who is Impacted?

AML regulations require financial institutions issuing credit or allowing customers to open accounts to complete due-diligence procedures to ensure they are not aiding in money laundering activities or financial crimes. These companies must practice enhanced due diligence and ensure their customers are not taking part in a money laundering scheme. They must also verify where large sums of money originated, monitor financial transactions and report suspicious activity.

How Jumio Can Help

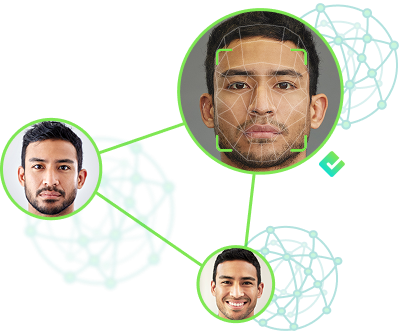

- Jumio Identity Verification automates the online identity verification process to ensure the person is who they say they are while providing a frictionless onboarding experience.

- Jumio Screening lets you adopt a risk-based approach by screening your customers against PEPs, sanctions, adverse media and other watchlists.

Verify customers across the globe: countries, languages, ID types

Instant feedback to improve conversions and reduce drop-offs

Verify customers across devices: Native mobile, web, mobile web, API

Extract proof of address from utility bills, bank statements, and credit card statements

Fast and easy customer experience

Ready to see how Jumio can help you achieve AML compliance?

Trusted by leading brands worldwide.

VP of Digital Experience Alaska Airlines